CDSL Share Price Target : Central Depository Services Limited (CDSL) stands as a backbone of India’s capital market infrastructure, enabling digital securities transactions for millions. As the stock attempts a comeback from recent corrections, investors are asking: Can CDSL reach and break past Rs 2,900 in 2025?

Let’s analyze the stock in two parts – technical and fundamental.

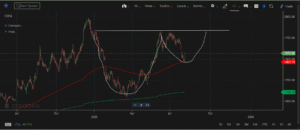

1. Technical Analysis: Cup with Handle Pattern in Focus

Pattern Analysis:

The chart above illustrates a classic “cup with handle” formation—one of the most reliable bullish continuation patterns in technical analysis. Here’s how it shapes up for CDSL:

-

The Cup:

The share price formed a broad, rounded bottom from its previous high (~Rs 1,990) down to ~Rs 1,050, then gradually recovered. This curved base signals that sellers have been exhausted and buyers are regaining control. -

The Handle:

After the recovery, a consolidation (minor dip) has formed—the “handle”—usually a healthy pause before a breakout. This often shakes out weak hands and accumulates strength. -

Key Resistance:

The neckline or breakout point sits around Rs 1,990. Sustained trading above this level would confirm the completion of the cup with handle pattern, typically leading to a strong upside. -

Upside Target Calculation:

The height of the cup (~Rs 1,990 – Rs 1,050 ≈ Rs 940) is often projected upwards from the breakout:

Target = 1,990 + 940 = Rs 2,930

The next major psychological level is Rs 2,600, well within this range.

Moving Averages & Support:

-

The red line (200 DMA) around Rs 1,467 offers strong support.

-

The green line (likely 400 DMA) at Rs 1,108 signals the long-term trend remains intact.

Summary:

If CDSL can break and hold above Rs 2,000 with volume, there’s a solid technical case for a run toward Rs 2,600–2,900 in 2025.

2. Fundamental Analysis: Is the Growth Story Intact?

Business Overview

-

Core Offering:

CDSL is a Market Infrastructure Institution providing demat, securities settlement, e-voting, and KYC services, critical to every capital market participant from retail investors to institutions.

Financial Highlights (August 2025)

| Metric | Value |

|---|---|

| Market Cap | ₹32,863 Cr |

| Current Price | ₹1,572 |

| 52W High/Low | ₹1,990/1,047 |

| P/E Ratio | 66.5 |

| Book Value | ₹84.2 |

| Dividend Yield | 0.60% |

| ROCE | 42.0% |

| ROE | 32.7% |

| Piotroski Score | 7.0 |

| Industry P/E | 49.4 |

Business Segments & Revenue

-

Depository Services (79% of revenue): Dematerialization, holding, and transfer of securities, plus e-voting.

-

Data Entry & Storage (20%): KYC and record-keeping.

-

Repository (~1%): Insurance and commodity document digitization.

Market Position & Expansion

-

Clients: Grew from 1.08 crore in FY16 to over 10.5 crore in 2025, showing massive digital adoption.

-

Network: 580+ depository participants across the country, strong brand trust.

-

Subsidiaries:

-

CDSL Ventures: India’s first and largest KRA.

-

Insurance Repository: Partners with 35 insurers.

-

Commodity Repository: Pioneering in electronic commodity asset transfer.

-

Growth and Profitability

Key Pros:

-

Debt-free balance sheet (Borrowings: ₹3 Cr; Reserves: ₹1,551 Cr).

-

Stellar profit growth (last 5 years: 37.8% CAGR, last 3 years: 19% CAGR).

-

Consistently high ROE (10-year avg: 25%; Last year: 33%).

-

Healthy dividend payout (55%).

Seven-Year Profit Growth (Cr):

-

Net Profit: 115 → 526 Cr (CAGR of 31%)

-

Operating Profit: 109 → 600 Cr (sustained OPM improvements)

-

Compounded sales growth remains above 25% for both long and medium term.

Risks

-

High P/E (66.5 vs industry 49.4) points to premium valuation; future returns hinge on sustained profit compounding.

-

Regulatory and technology risks inherent in capital market infrastructure.

-

Any dip in market activity can dent transactional revenues.

Conclusion: Will CDSL Hit Rs 2,900?

Technicals:

A textbook cup with handle suggests a high probability of a breakout to new highs if Rs 2,000 is breached with conviction. Target: Rs 2,600–2,900 in 2025.

Fundamentals:

Top-tier financial health, market dominance, and strong profit/sales momentum justify a premium-but keep an eye on valuation and broader market sentiment.